NAB’s June Business Survey was undertaken right amidst the heightened uncertainty around the Brexit referendum, and ahead of the Australian Federal election.

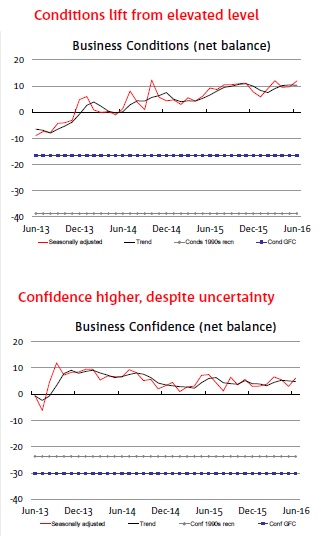

Despite this, firms in the Survey continued to report very high business conditions, pointing to another strong quarter for the non-mining economy. The business conditions index rose from an already elevated level, hitting +12 index points in June, which is consistent with the post-GFC highs for the series.

Encouragingly, the improvement was driven in large part by a lift in employment conditions, which are back above long-run average levels. Profitability also improved in June, while trading conditions (sales) were unchanged at very high levels.

According to Alan Oster, NAB’s Chief Economist, “we are very much seeing a continuation of the positive trends evident in the Survey for some time now.”

Overall, business conditions were up 2 points to +12 index points in June, which is well above the long-run average of +5. On the components of business conditions, Mr Oster noted that “strong activity seems to be having a positive effect on labour demand in the Survey, despite recent “questionable” official labour market statistics suggesting otherwise”.

By industry, there is still some (albeit mixed) evidence in the Survey that improvements in the non-mining economy have become more broad-based, while mining also looked a little better. Indeed, most industries reported a rise in business conditions this month, although retail was a notable exception.

“The deterioration in retail coincides with big declines in retail price growth, highlighting the competitive and cost pressures facing the industry” said Mr Oster.

“However, we should be able to take comfort in the trends we are seeing across many other industries”.

In fact, even though the Survey was undertaken during the worst of the volatility in financial markets post the Brexit vote, business confidence actually improved – rising 3 points to +6 index points.

According to Mr Oster, “this suggests that firms are looking through external uncertainties, choosing to focus on the positives they see in their own business, at least for the time being”. He goes on to say that “it is encouraging to see firm’s sentiment is holding up, particularly as we head into a period of political uncertainty.

Leading indicators from the Survey are looking reasonably good, with forward orders and capex both improving, although spare capacity rose as well – probably reflecting rising capacity, rather than falling demand. “These results generally tell us we can be confident about the near-term outlook”, said Mr Oster.

Overall the Survey suggests the RBA should be reasonably comfortable with the present state of economic activity, even in the wake of recent events that cloud the outlook. However, the view on inflation is arguably more important at this juncture, and the Survey is not suggesting any meaningful turnaround in near-term inflation pressures.

These trends justify the highly accommodative setting for monetary policy, but while the August RBA meeting (post Q2 CPI) is likely to be ‘live’, current information suggest rates will remain on hold (although it is likely to be a close call).