NAB’s Chris Sheehan on why Australia’s comprehensive, preventive approach to tackling scams is more sophisticated and more effective than any other country.

Australia is a world leader responding to the scams epidemic, a fact recognised by other countries who are envious of what we are achieving and eager to learn from our experience.

That’s my key conclusion from two recent trips to London, where I met with representatives of major UK banks, government, regulators and industry associations and attended the Global Anti-Scam Summit with colleagues from the Australian Banking Association (ABA) and the Australian Financial Crimes Exchange (AFCX).

A UK-style model isn’t stopping scams at the source, actually

The iconic movie Love Actually described Britain as the country of Shakespeare, Churchill, the Beatles, Sean Connery, Harry Potter. David Beckham’s right foot. David Beckham’s left foot.

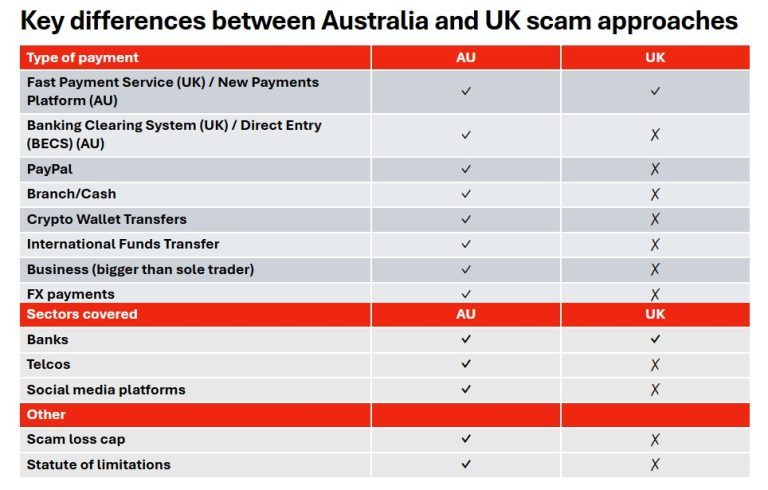

It’s also known for its mandatory scam reimbursement system. Under laws that came into effect in October 2024, banks must reimburse customers who lose money to scams within five days.

This approach is often described as ‘world-leading’. But prevention is better than a cure. The UK model is focused on treating the financial symptoms of scams rather than seeking to stop them at their source. It does nothing to hold telecommunications or digital technology firms to account after a victim is hooked into a scam in the first place.

The Australian Scams Prevention Framework law, which passed Parliament in February, goes much further and will provide far greater coverage for consumers. It will capture more organisations and more payment types.